10. edition

18 June 2026

Key points from the World Bank Group’s Global Economic Prospects June 2026.

Source: Global Economic Prospects June 2026

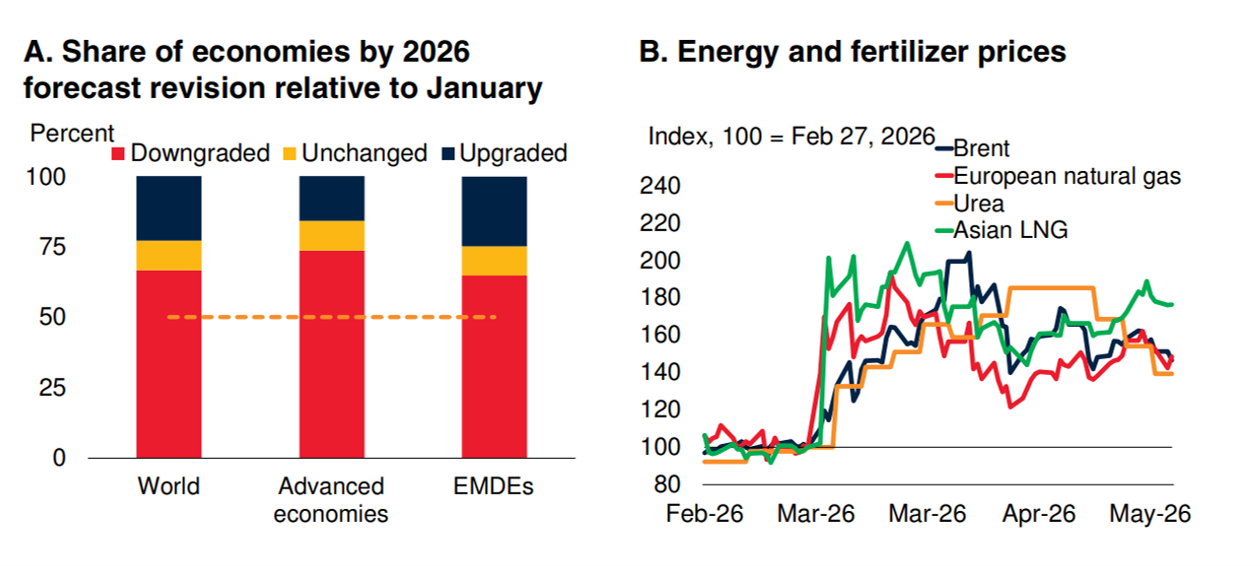

The conflict in the Middle East acts as economic shock, causing decline in trade volumes, increases in inflation with particularly high growth in energy prices, and expectations for tighter monetary policy.

As consequences, forecasts have been downgraded for about two-thirds of the economies worldwide. The global economic growth(real GDP) is forecasted to decline from 2.9% last year to 2.5% in 2026, the lowest rate since the COVID-19 pandemic. In case the energy supply disruptions remain and are complemented with serious financial stress, global growth could even drop to 1.3% in 2026. For 2027-28, global growth is expected to reach 2.8% respectively.

Advanced economies are expected to slow from 1.8% in 2025 to 1.5% this year, and back to 1.8% and 1.7 % for the coming two years. Emerging and developing economies are projected to slow from 4.4% last year to 3.6% in 2026, with growth potential of 4.2% and 4.1% for 2027-28. Out of all the regions for this year, the highest growth of 6.3% is projected in South Asia (SA) and the lowest growth of 1.6% in the Middle East, North Africa, Afghanistan and Pakistan (MENAAP).

Global inflation is expected to reach 4%, in particular commodity prices to rise by 22% in 2026. In 2027 inflation is forecasted to drop to 3.3% and further to 2.9% in 2028.

Public debtlevels are about to reach highest levels in decades in the emerging and developing countries, averaging at 70% of GDP. About 60% of the low-income countries are already in or close to debt distress.

Based on the report’s findings, I believe that the global economy is experiencing a stretched economic stagnation and instead of chasing growth, we must focus on structural shifts for increased resilience and sustainability, which could include diversifications, productivity enhancements, and targeted investments.

Do you want to learn more? After the first session of ‘Trends Beyond Hype’ Series with policymakers, I invite the business community to sign up for the second session on the 16th of July at 14:00 CEST to discuss geoeconomic trends and their implications.