5. edition

16 March 2026

What is at stake for the global economy at the Strait of Hormuz and in the Gulf Cooperation Council (GCC) region?

In foresight terminology, we use the term ‘wildcard’ for an event, such as the US-Israel-Iran war, with low probability but very high impact. Here is my brief overview about the impacts, based on the global economic share of the GCC countries and trade flows via the currently closed Strait of Hormuz. Starting with a few key facts (data from UNCTAD, GCC Statistical Center, IATA):

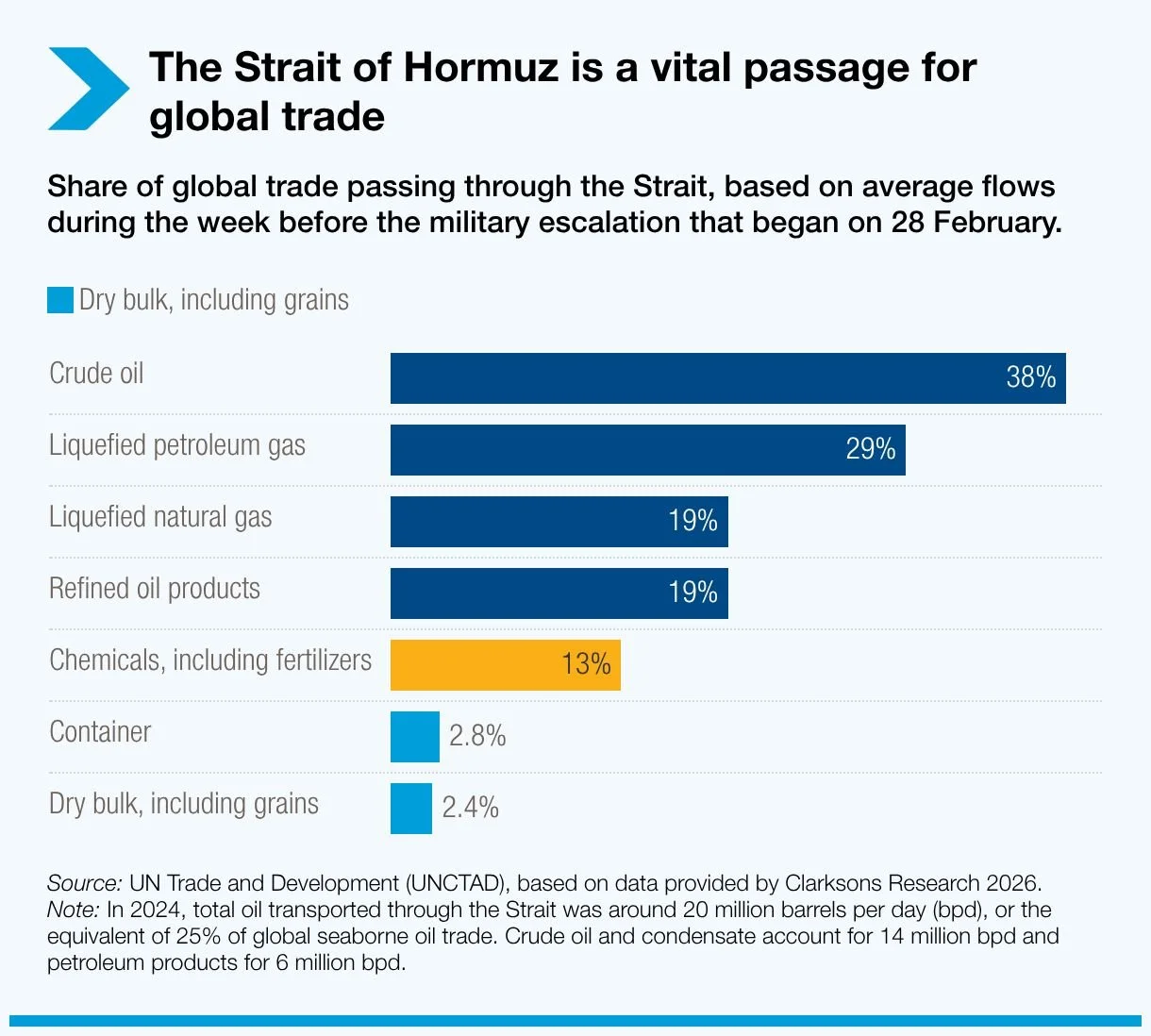

Out of the total global seaborne trade, 38% of crude oil, 29% of Liquified Petroleum Gas, 19% of Liquified Natural Gas, and 13% of fertilizers are shipped through the Strait of Hormuz.

The destination of the majority of exports from the Arabian Gulf is Asia, with China, India and Japan being top trading partners.

Most of the imports of the GCC countries pass through the Strait of Hormuz, including 70% of food being shipped via the Strait.

About 13% of global air cargo volumes are from the Middle East.

Short-term implications, among others, include increases in the price of oil and gas, other energy products, fertilizers; transport and insurance costs. Rise in the price of food and food shortages may occur, with the potential for surge in the cost of living in most countries globally as price increases spiral through the supply and production chains.

I also have a strategic observation to share for mid to long term. When the Covid19 pandemic hit and the global economy and supply chains were grounded for months, the world finally came to realize that the overdependence on Chinese manufacturing may need to change. Since then, we can observe the actions of restructuring, diversification and nearshoring. Now, with the closure of the Strait of Hormuz, the choke point for fossil fuels and fertilizers trade, I expect supply chain diversification efforts to be further enhanced and the overdependence on imports to be reduced over time.